Commentary

Rail Equipment Expert Panel Takeaways

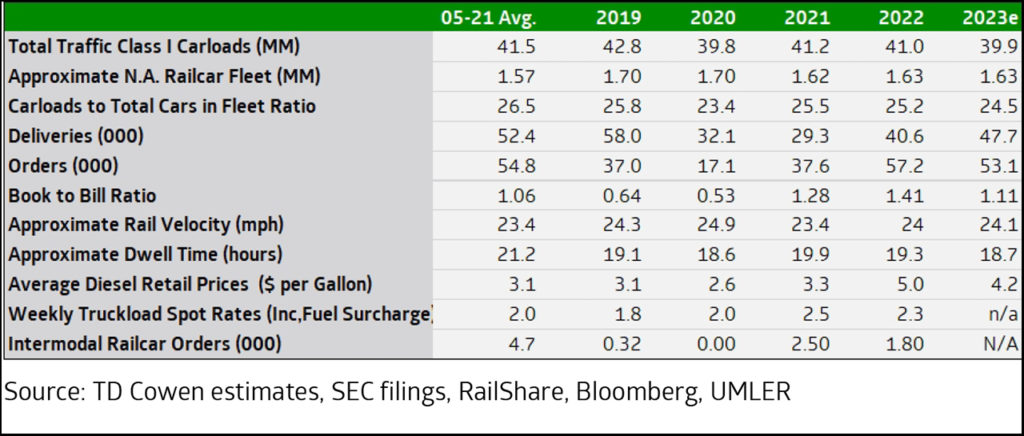

Written by Matt Elkott, Jason Seidl, Bhairav Manawat and Elliot Alper, TD CowenRailcar manufacturing inquiries and orders appear to have moderated, but the 2024 build outlook remains stable, modestly above replacement demand. Lease rates are holding up well at elevated levels. While locomotive parkings could increase in the coming months, the modification cycle remains intact. Relative to a couple of months ago, the expert panelists’ tone was neutral to slightly more cautious.

- We see the takeaways as neutral to slightly cautious, perhaps more so for manufacturing than leasing. This is largely consistent with the results of our January 17 4Q23 Rail Equipment Survey, in which a mildly lower percentage of respondents relative to our 3Q23 survey said they planned to order railcars in the next 12 months.

- The panelists see rail velocity continuing to improve, and noted that, coupled with weak rail traffic, this could lead to more locomotive parkings, but not significant numbers beyond what has already occurred.

- One of our expert panelists believes the locomotive modification cycle, however, can withstand the challenging rail environment and should continue at healthy levels.

- Railcar inquiries and orders have decreased somewhat in recent weeks. This is because the need for railcars has eased a bit, not just because lead times are long.

- Rail traffic outlook remains challenged, but areas of potential upside could come from autos and intermodal later in the year.

- Intermodal could benefit from a shift to West Coast ports driven by the persistence of the Panama Canal’s low water levels. If the shift coincides with a rate recovery in truckload late in the year, there could be a meaningful uptick in intermodal.