UP 2Q24: Improved Results Across the Board

Written by William C. Vantuono, Editor-in-Chief

Union Pacific’s second-quarter 2024 results showed increases in volume, earning and income and improvements in safety, productivity and operating ratio. “Our performance demonstrates the team’s ability to deliver strong results,” said CEO Jim Vena. “This provides further proof that our strategy to be the best in safety, service and operational excellence will drive success. The entire Union Pacific team is energized behind this strategy and wants to win. As we build on the foundation we’ve laid over the past 12 months, we look forward to demonstrating what’s possible for our great company.”

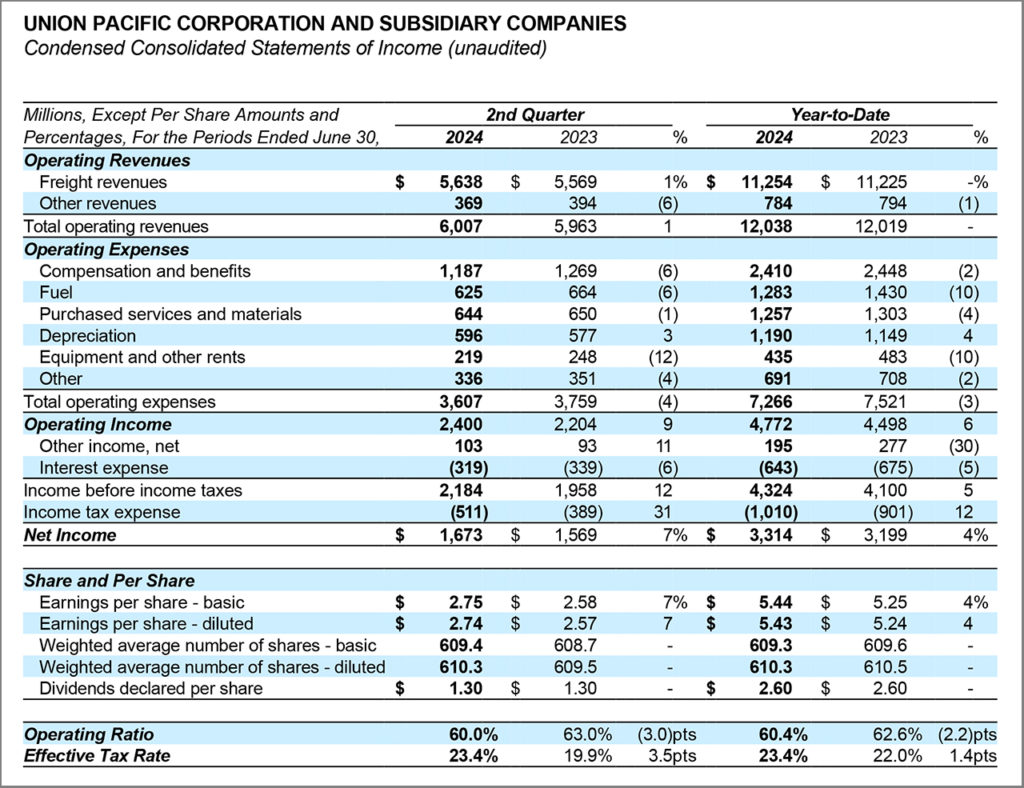

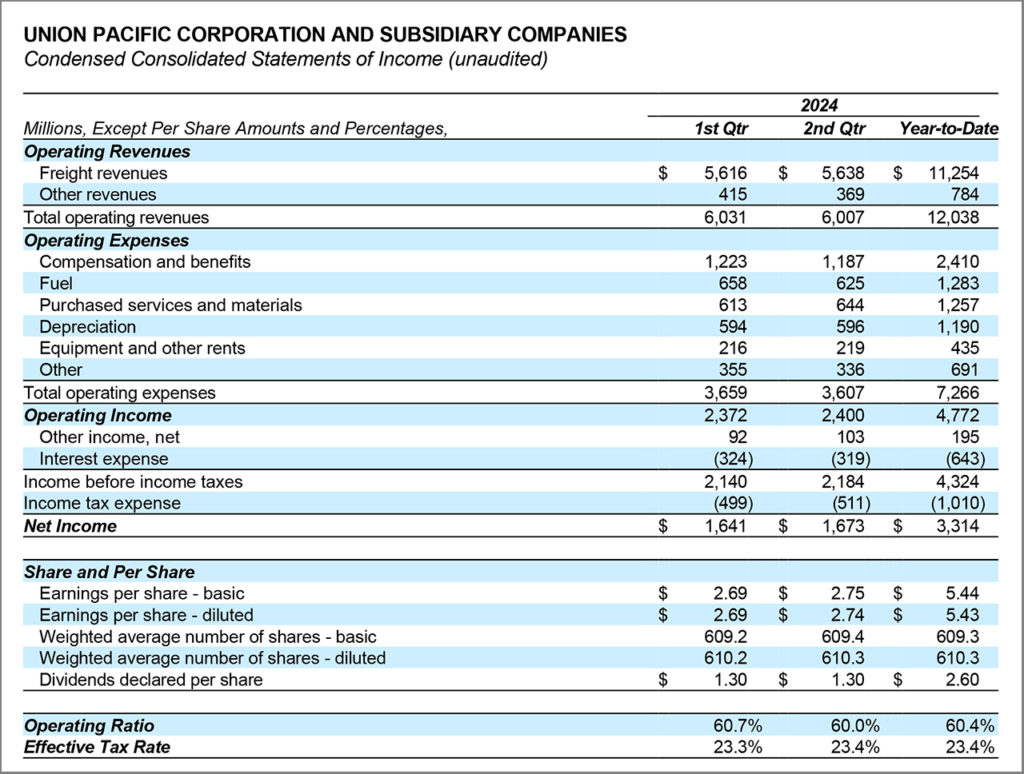

UP reported 2Q24 net income of $1.7 billion, or $2.74 per diluted share, compared to 2Q23’s $1.6 billion, or $2.57 per diluted share, based on “solid operating income growth driven by core pricing gains, increased volume partially offset by business mix and reduced fuel surcharge, operating efficiency and an intermodal equipment sale.” Operating revenue of $6.0 billion was up 1%. Freight revenue excluding fuel surcharge revenue grew 2% as revenue carloads grew “slightly.” The OR of 60.0% was an improvement of 300 basis points. Lower quarterly fuel prices and an existing environmental remediation compliance order negatively impacted the operating ratio 10 and 30 basis points, respectively. The intermodal equipment sale aided the operating ratio 70 basis points. Operating income of $2.4 billion was up 9%.

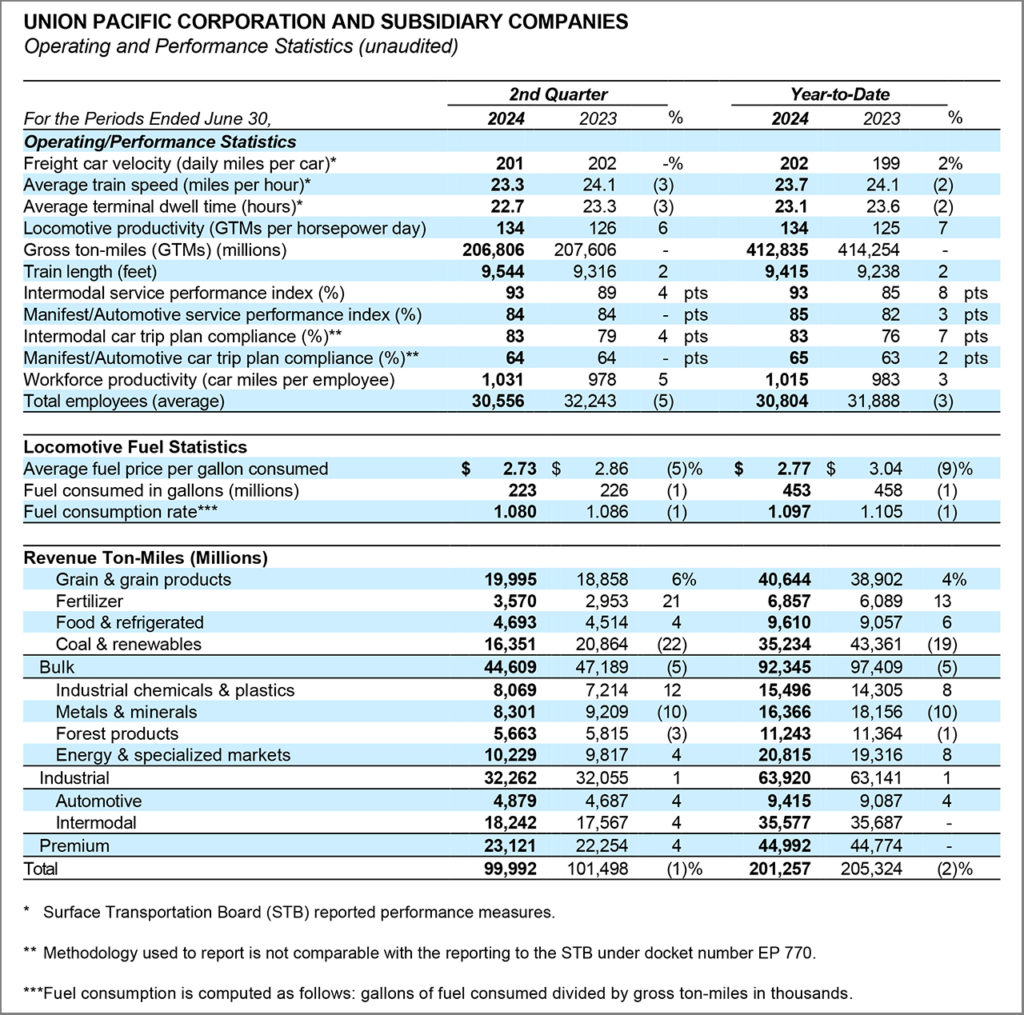

For a “network challenged by weather,” UP’s year-to-date reportable personal injury and reportable derailment rates both improved. Quarterly freight car velocity of 201 daily miles per car was flat. Locomotive productivity was 134 gross ton-miles (GTMs) per horsepower day, a 6% improvement. Average maximum train length was 9,544 feet, a 2% increase. Workforce productivity improved 5% to 1,031 car miles per employee. The fuel consumption rate of 1.080, measured in gallons of fuel per thousand GTMs, improved 1%.

For 2024’s second half, UP said the volume outlook “remains uncertain based on economic indicators and coal demand,” but the “profitability outlook continues positive momentum with a strong service product, improving network efficiency and solid pricing.” Share repurchases of ~$1.5 billion in 2024 were announced.

UP affirmed pricing dollars “in excess of inflation dollars,” no change to its long-term capital allocation strategy, and a 2024 capital plan of $3.4 billion. Next year’s capex, he told Railway Age, “will be close to that,” stressing that the railroad has “a multi-year base capital plan.”

“Our goal is to Get Consistently Better”

In an open letter, Vena thanked employees and provided examples of recently implemented Service Performance Index (SPI) metrics.

“Looking at our most recent quarterly results, I am very proud of how the team has continued to rise to the challenges that come with operating the largest railroad in North America, always expecting the unexpected, and looking for and delivering what is possible,” Vena wrote. “Thank you for another strong quarter.

“Looking back on the past year, the team is clearly proving we have what it takes to achieve what is possible. I’ve shared stories about why we will never compromise on safety. Year to date, we improved our reportable injury rate 20% and reportable derailment rate 15%. More important—more employees went home safe to their families, and our customers and communities experienced fewer disruptions. We rolled out a new safety strategy and are revitalizing our culture, enhancing our training and improving the way we communicate with our teams. All these efforts are part of our journey to be the best at safety. Nothing is more important, and we will never rest on this goal.

“I’ve spent the year speaking with many customers, who rely on us to deliver the service we sold and keep our promises. They are frank about when we do, and when we don’t. We introduced a new metric, Service Performance Index (SPI), that challenges us to ensure the service customers receive today matches up against our best performance over the past three years. Our goal is to get consistently better, and we are. Over the past 12 months, Manifest SPI improved 7.2 points and Intermodal SPI improved 11.4 points.

“Our customers and regulators share our service goals and expect us to keep delivering reliable service, and to prove it over time. I have no doubt we will. They are also counting on operational excellence, which means we must have a buffer—with people and equipment ready for inevitable weather events, unexpected outages or supply chain challenges. During the past year, we’ve recovered from events and incidents more quickly, getting service back on track and keeping the railroad fluid. Cars are moving 6% faster, train speed is up 9% and car dwell is down 4%. Our strong Union Pacific team is at the heart of all these results. Because of our people, locomotive productivity is up 9% and train size grew nearly 2%. You continue to stretch and prove what is possible.

“I’ve met with hundreds of stakeholders since my return to Union Pacific, including elected officials, regulators, shareholders and employees. Our people and our culture are very important. I’ve enjoyed some of our proudest moments in rail yards, offices and on the road, from touring the Big Boy, to celebrating the launch of NetControl, to testing our first-of-its-kind hybrid battery-electric locomotive. I’ve met you working in tough conditions, in temperatures below freezing and over 100 degrees. I know from experience how hard your jobs are, and I appreciate your sacrifices and tremendous efforts.

“As I look at the next year ahead, I am listening to your feedback about what we need to do to keep getting better. I said from day one I would ask a lot of you, and demand even more from myself. The year has truly flown by, and I am honored to have the responsibility of leading this great team and this historic railroad. You continue to prove what we can accomplish when we work together—and to show the world what is possible for Union Pacific. I look forward to what we will accomplish next.”

The “buffer” involving people and equipment Vena referred to enables the railroad to recover quickly from operational interruptions caused by extreme heat or cold, wildfires, landslides, tornadoes, hurricanes, flooding, etc., which have gotten worse in the past few years and are no longer considered anomalies. “Railroading is an outdoor sport,” he told Railway Age. “We know we’re going to get impacted, and we’ve experienced more than our fair share. We’re looking for more flexibility from our agreement employees to be able to respond and recover. In the next round of collective bargaining, I’ll be looking to incorporate some additional flexibility into our labor agreements.”

TD COWEN INSIGHT: UNP OVERCOMES 2Q CHALLENGES; 2H VOLUME OUTLOOK SOMEWHAT MUTED

By Jason Seidl, Wall Street Contributing Editor

UNP ~met expectations in Q2 and showed sequential margin improvement that should continue into 2H24. Top line outlook remains uncertain as management struck a more cautious demand tone and slightly softer pricing despite easier comparisons, in our view. We are encouraged to see UNP lean into stock buybacks in 2H. Our price target moves to $255, reiterate Buy.

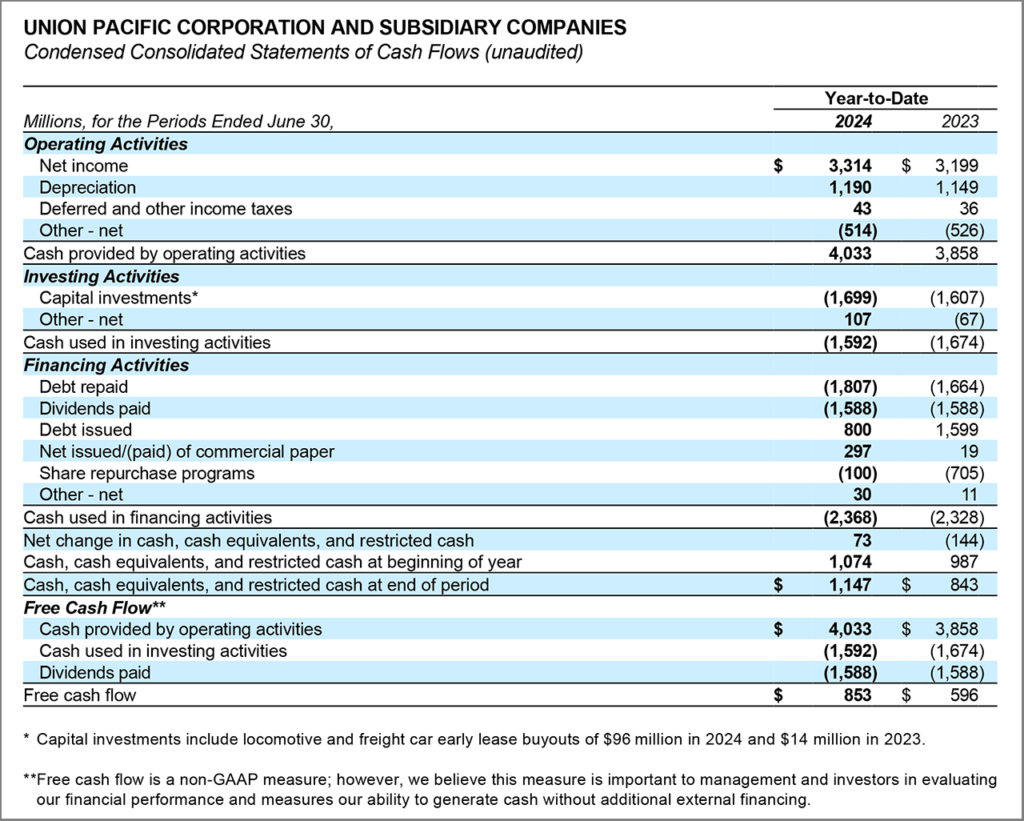

UNP reported 2Q EPS of $2.74 and a 60% OR, which includes a 70bp gain from an intermodal equipment sale and a 30bp drag from an environmental charge resulting in a net $0.04 to the bottom line. Excluding these one-time items, EPS was slightly below our estimate but in-line with the Street forecast of $2.70 while OR is slightly worse than our estimate. UNP resumed its share repurchases in 2Q, buying back $100MM of stock.

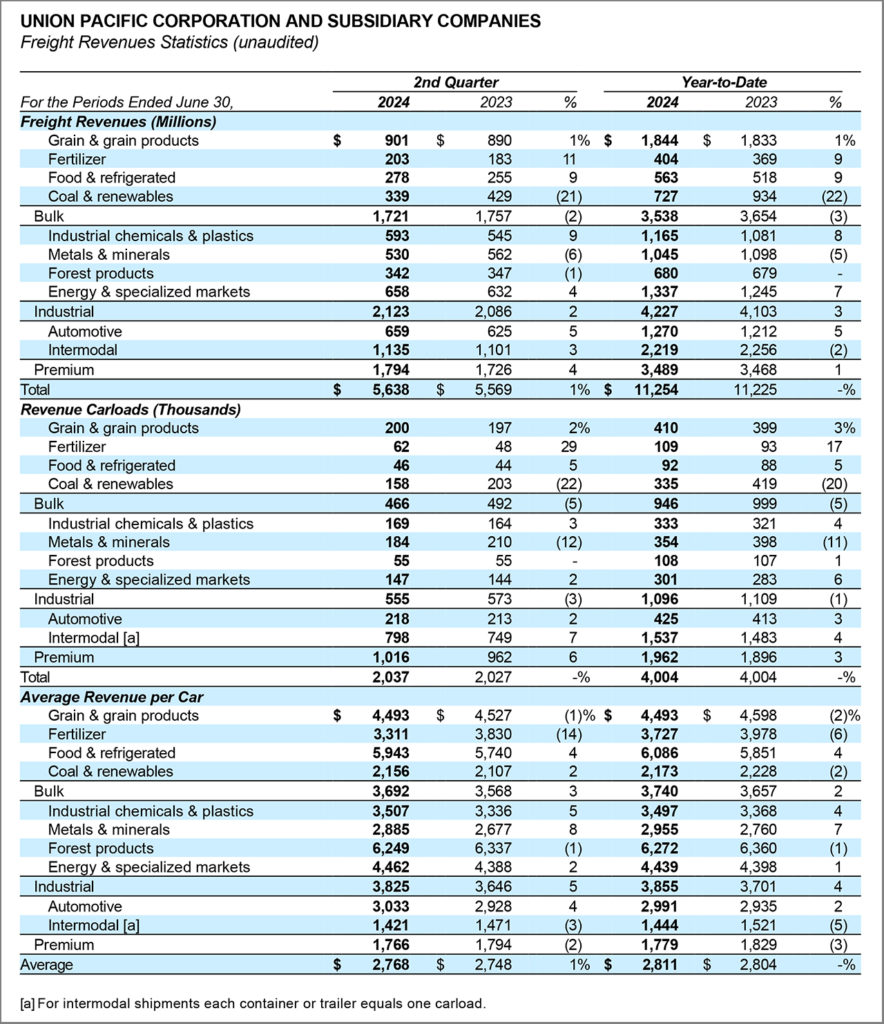

Strength in bulk and intermodal volumes up 6.6% y/ and 6.5% y/y respectively in 2Q was offset by a large 22% decline in coal volumes that are well understood. UNP sees an uncertain volume backdrop in 2H driven by macro softness and continuation of the secular decline in coal. Industrial volumes were –3.1% y/y in 2Q and management sees broad softness continuing. International intermodal should continue to see strength on robust import volumes and UNP is seeing some transloading to domestic intermodal.

Consolidated revenue/carload +0.7% missed our estimate in 2Q. Intermodal yields –3.2% sequentially came in lower than we expected and exacerbated mix pressures in the quarter. Mix pressures should persist into 3Q with intermodal leading carload growth. While management pointed to some clawback on pricing with customers, we do not get the sense that this has intensified across the book of business yet. Commentary tracks with findings of our quarterly shippers’ survey pointing to a fairly modest uptick in pricing expectations. Note that ~50% of UNP’s book is comprised of long-term contracts.

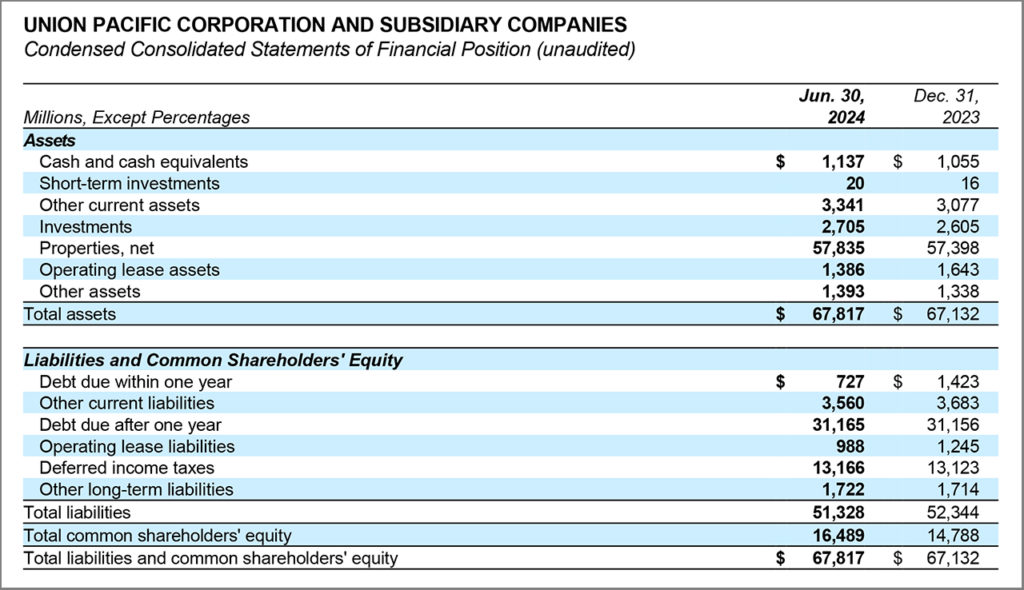

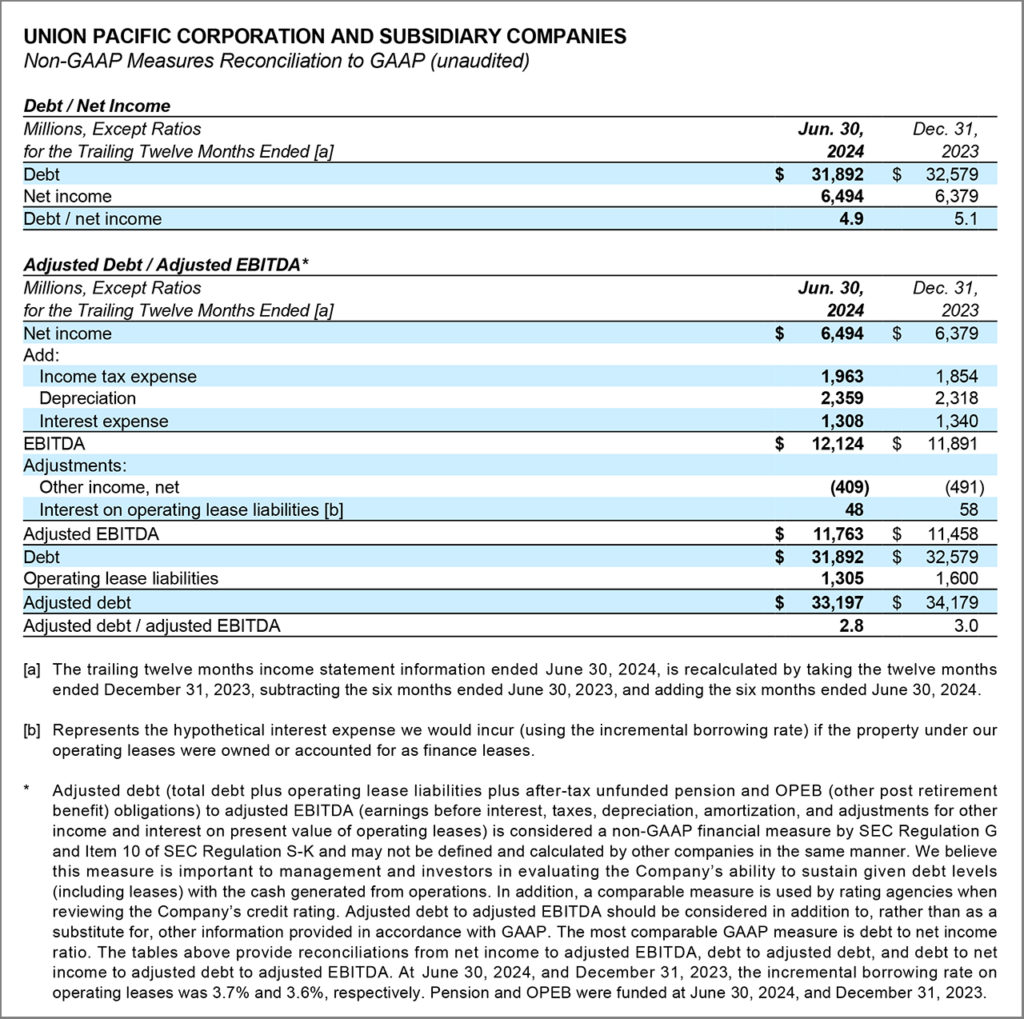

After announcing the resumption of buybacks last quarter, UNP repurchased $100MM of shares in June, and now expects to repurchase $1.5B worth of shares in 2024, materially stepping up in the back half of the year. UNP expects net leverage to stay ~flat at 2.8x through the remainder of the year after stepping down marginally sequentially. We increase our buyback assumptions into 2025.

UNP reduced its headcount 5% in the quarter with flat freight car velocity despite some material weather events in the quarter. Train service employees increased 1% while the remainder of the workforce declined by 9%. UNP continues to create a leaner network as it works to offset some increased impacts from labor agreements. Operationally, the company overcame some weather challenges in 2Q and should set up well for 2H barring any unforeseen events.

We lower our 2024 and 2025 EPS estimates to $11.10 from $11.25 and $12.75 from $12.95, respectively. Continuing to use our 20x multiple, our price target moves to $255; reiterate Buy.