Commentary

‘There Will Be Hell to Pay’

Written by Robert H. Cantwell, Contributing Editor

William C. Vantuono photo.

During a 2013 GATX earnings call, then-CEO Brian Kenney was asked a question about the staggering number of new railcar orders being placed in response to the crude-by-rail/fracking boom. His response was something I’ll never forget: “If all of these cars are delivered, there will be hell to pay.”

Kenney was right. In 2014 and 2015, all the railcar builders scrambled to ramp up capacity to build 80,000 cars in 2015. It was controlled chaos, and very profitable. However …

There are now more than 120,000 tank cars and frac sand cars in storage. Entire plants have been shut down, taking out considerable capacity. Nascent leasing companies came and went. The carbuilders have since struggled to return to acceptable profitability while the industry benefited from their over-capacity and restructurings. Again, Kenney was right: Railcar builders have been going through hell since 2015. And just as they’ve been recovering, recent orders have begun to fall to levels far below replacement levels.

ARCI Q42023 orders came in at 4,164, while Q12024 orders came in at 5,864. This is against deliveries of 11,000/quarter. We’re not living in a crisis like 9/11, the Great Recession or COVID, but we’re ordering new railcars as though we are.

Given the many changes in railcar production capacity through years of rationalization, car owners will likely be surprised in the very near future by extended lead times and higher prices when they do decide to order.

Railcar Replacement Demand

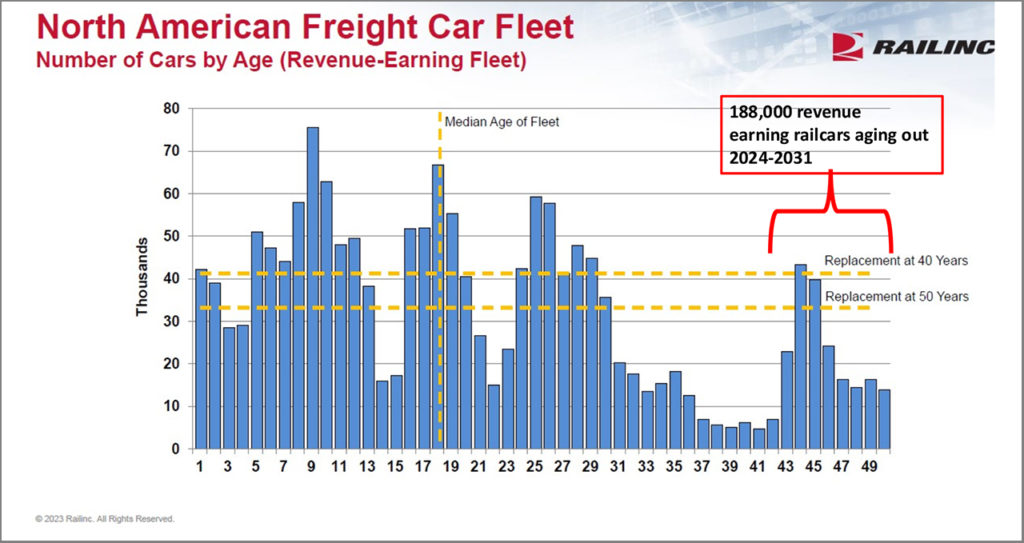

Every discussion surrounding the current railcar demand environment focuses on “replacement demand” levels. There is debate as to what replacement demand is. Dr. David Humphrey of Railinc produces a railcar aging chart that is very useful in projecting railcar replacement trends. In his chart, he reflects a 33-35,000 replacement number, based on a 50-year life. But at a 40-year life, replacement demand jumps to 41-43,000/year. Looking closer at the chart reveals a mountain of retirements facing the industry over the next seven years—and these are revenue earning cars. There are an additional 300,000 railcars in storage, many of which will likely not return to service and will face the scrap heap.

In addition to the scrapping detail above, the S-259 fleet, railcars that were produced between 1995 and 2004 and have been loaded to 286K GRL, will likely see their numbers decline as maintenance expense increases. There are approximately 358,000 cars in the S-259 fleet.

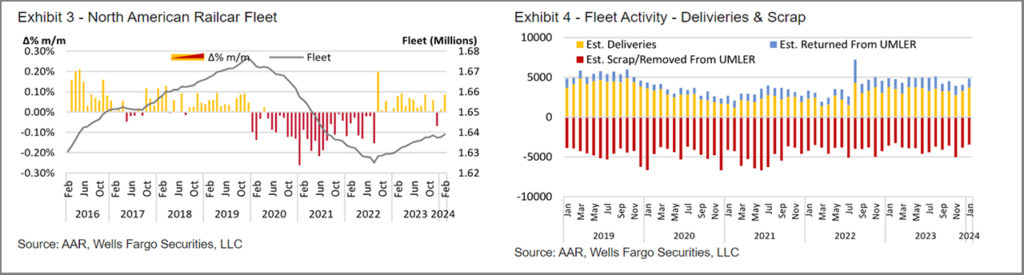

Railcar scrapping has been elevated for the past five years, ranging from 3,500-5,000 /month – far outpacing new railcar deliveries. As a result, the total fleet has shrunken from almost 1.68 million to 1.63 million today. With elevated scrap steel prices and a fleet that is aging out, expect this pace to continue, and likely increase.

Wells Fargo Financial and AAR do a great job tracking fleet size and scrapping vs. new car production:

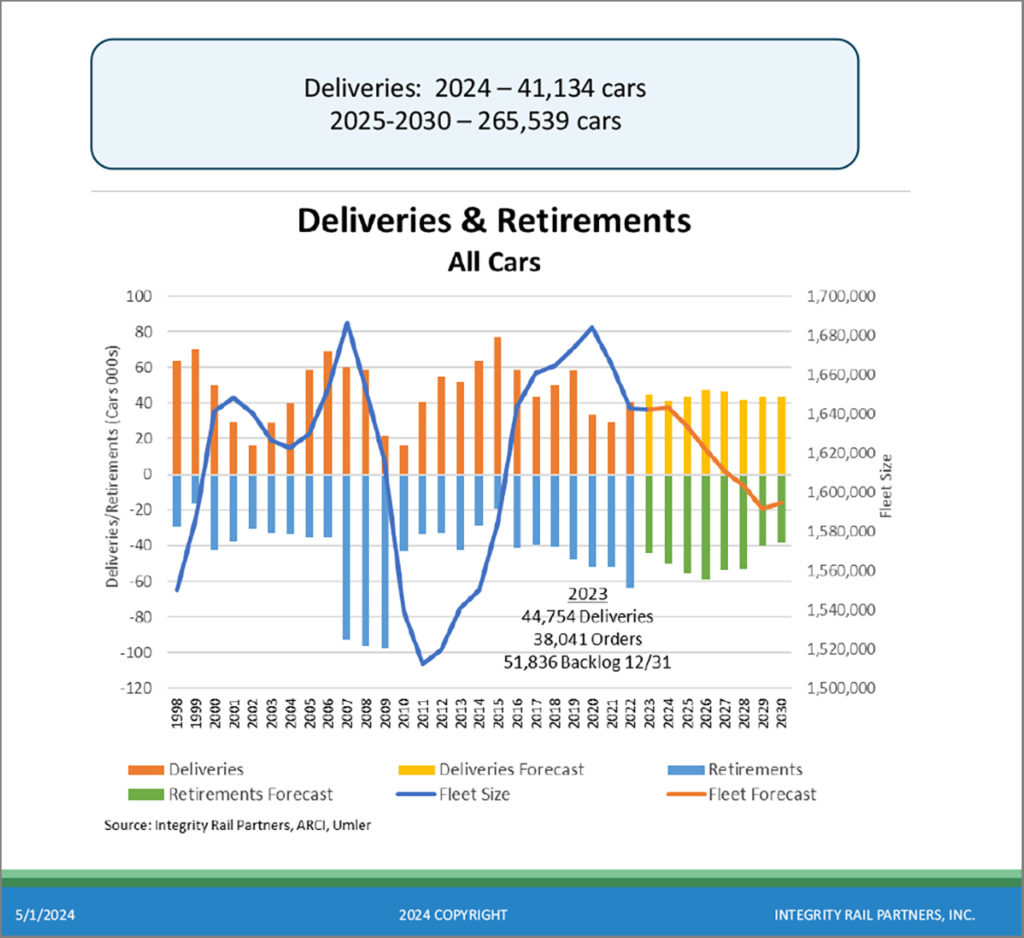

Dick Kloster, President of Integrity Rail Services, has developed a projection based on these anticipated scrap rates that reflects the need for annual deliveries to exceed 42,000 railcars for the next five years—and even then, the fleet will continue to shrink:

Railcar Building Capacity

As outlined in my previous articles, there has been a seismic shift in the railcar building market. The industry has shrunk from seven builders to five today, dominated by two large builders, Greenbrier and Trinity. This consolidation has resulted in railcar assembly capacity rationalization. Today, there are 11 assembly plants, down from 19 in 2015 when the industry built a whopping 80,000 railcars. Keep in mind that this number included 35,000 tank cars, which are now trending around their historical 10-12,000 annual production rate.

Industry-wide, there are 41 active assembly lines, including Freightcar America’s recent line additions (4) at their new plant in Castanos, Mexico. Of these 41, 10 are dedicated to tank cars. There are a handful of idled lines that offer some “flex capacity,” but this amounts to approximately 5-7,000 additional railcars—if you can find the people to produce them. Assuming each line has a capacity of 1,250 cars/year on average, the resulting industry theoretical capacity is about 51,250. But with product mix and line changeovers, a more realistic industry capacity is 47-49,000 cars/year—close to our current run rate

Since some capacity (25%) is dedicated to tank cars, which are in low demand and likely to stay that way for a very long time, repurposing tank car lines to build other car types isn’t feasible. Most tank car lines have been idled or permanently closed. The industry no longer has the ability to come close to producing the 35,000 tank cars built in 2015, nor will they need to.

Railcar builders have struggled to achieve a 10% gross margin on their railcar sales since the halcyon days of 2015. With low returns on railcar building combined with elevated interest rates, don’t expect new capacity to be added anytime soon.

Leasing Environment

Lease rates have continued their upward trend while lease terms are extending beyond 60 months. While this is car type-specific, overall the leasing market remains very robust. Lessors benefit from markets with tight railcar availability. For a more detailed review of the current leasing market, see David Nahass’ Guide to Equipment Leasing in the June issue of Railway Age, “Moving More with Less.” In the article, he raises the question of the preparedness of the industry once demand increases beyond replacement levels. Based on the capacity discussion above, the answer to this question is: When demand rebounds, expect to wait!

Railcar Loadings/Growth on the Horizon?

Recent railcar and intermodal loadings are up 1-3%, even as coal continues its downward descent. After flat overall loadings for the past 25 years, the industry continues to innovate away from its dependence on coal, relying heavily on new railcar designs to fill market needs. While we remain focused on “replacement level demand,” we should begin contemplating potential growth needs to our calculations for railcar demand. This too will strain existing capacity.

As the industry pivots to growth, fleet capacity and railcar availability are important variables that impact the ability to service customers and grow carloads. Since the fleet has shrunken from 2015, continued shrinkage will limit overall growth potential. While railcar scarcity will benefit lessors, it will likely negatively impact the overall industry.

Summary

The current order trend makes little sense, given the outlook for railcar scrapping, tight availability for many car types and the potential for carload growth. As demand rebounds, there will likely be an outcry for more responsive deliveries and shorter lead times, but with current low margins on new railcars, adding more capacity isn’t justifiable. After everything railcar builders have endured since 2015, they will be seeking better returns and will be far more disciplined when considering capacity decisions. For car owners, you should anticipate your railcar retirements now, and order replacements sooner rather than later. If car owners wait too long to rebuild their fleets, with orders way below replacement levels, there will be hell to pay—only this time, it will be to the detriment of the entire industry.

Principal of Rail Supply Chain Associates, Robert H. Cantwell spent more than 40 years in executive positions in the rail supply industry. He spent the first 26 years of his rail industry career growing a successful company, Hadady Corp., a designer and manufacturer of truck (bogie) components and systems for locomotives and transit railcars. Following the sale of his business, Bob helped transform Amsted Rail, holding various executive positions for 16 years. He has been active in the Rail Transportation Division of the ASME (American Society of Mechanical Engineers) and is past Chairman of the Division. Bob holds degrees in Mechanical Engineering from the Georgia Institute of Technology and an MBA from the University of Chicago. He possesses a unique perspective on the rail supply industry, combining his engineering experience along with robust economic and financial acumen. As an active investor in the rail industry, he has a vested interest in the success of the industry. He has also actively advocated with members of Congress in support of the rail and rail supply industry. The opinions expressed here are his own.