CSX: ‘Solid Earnings Growth’ for 3Q22 (Updated, Cowen)

Written by Marybeth Luczak, Executive Editor

“CSX faced operational challenges to start the year, which contributed to first quarter results that did not meet our expectations.” –President and CEO Joe Hinrichs. CSX photo.

“I would like to thank Jim Foote and the entire CSX team for delivering another quarter of solid earnings growth,” CSX President and CEO Joe Hinrichs said during the Class I railroad’s third-quarter financial report, his first since taking the throttle from Foote in September. “I am tremendously excited to work with all the railroaders who make this performance possible and to lead an organization that is fundamentally committed to operational excellence.”

Following are highlights of CSX’s third-quarter 2022 results:

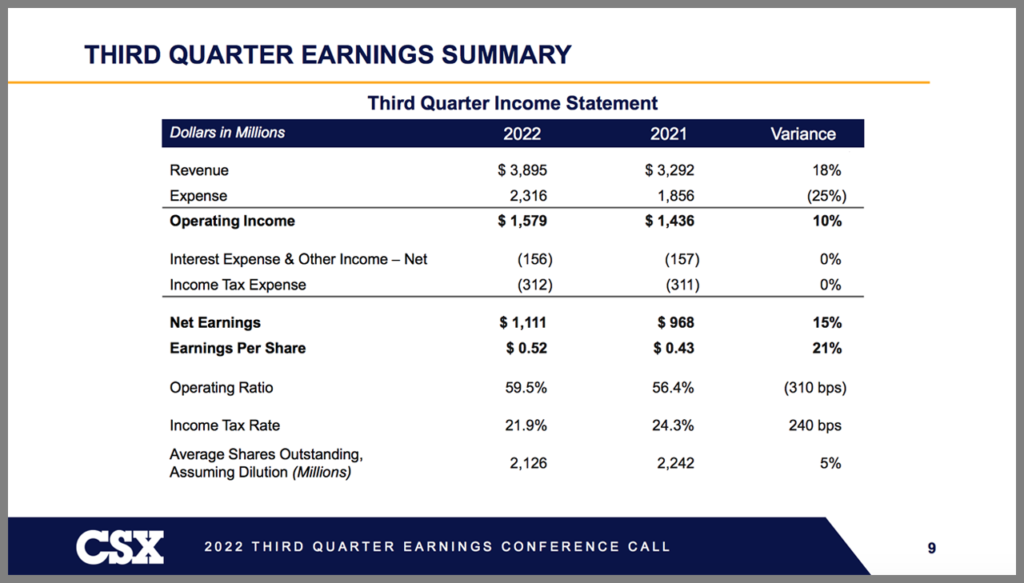

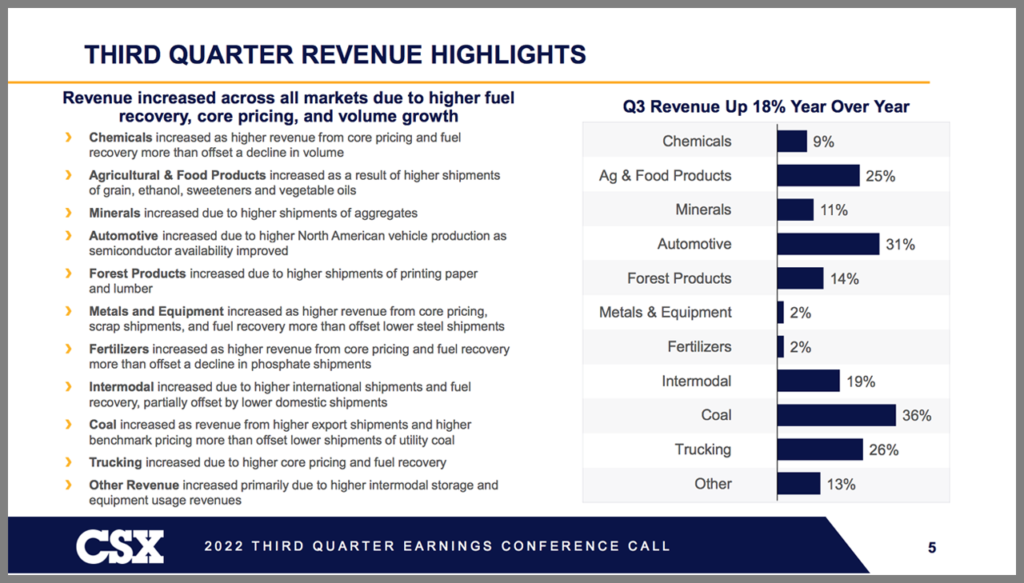

• Revenue reached $3.90 billion, increasing 18% year-over-year, “driven by higher fuel surcharge, pricing gains, a 2% increase in volumes [which reached 1,587K], and an increase in storage and other revenues,” according to CSX.

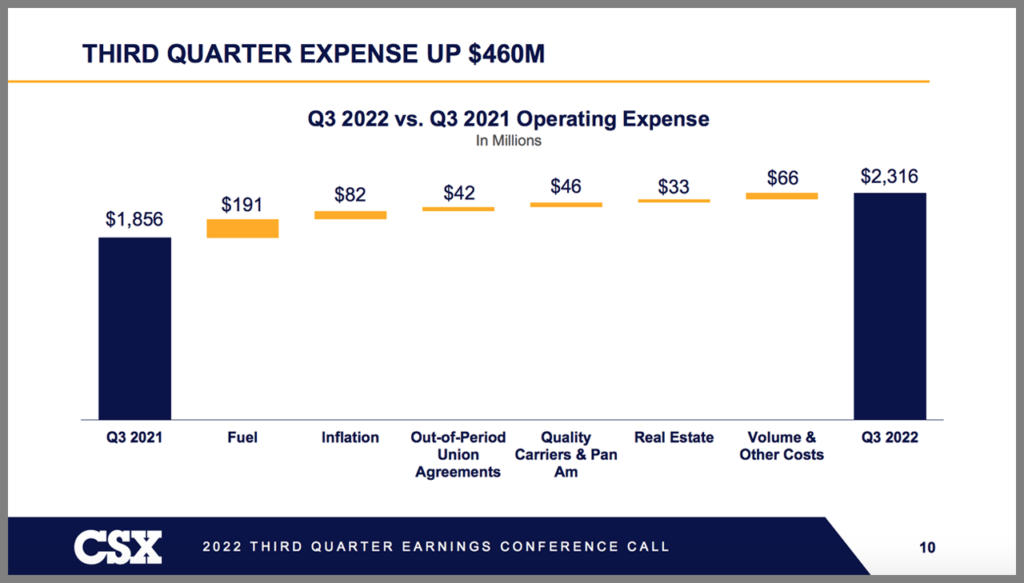

• Operating income came in at $1.58 billion, up 10% from the prior-year period’s $1.44 billion. “Third-quarter results include additional labor and fringe expense related to tentative union agreements, with $42 million specifically to adjust for wage, bonus, and other benefit costs in prior periods,” according to the Class I railroad.

• Net earnings of $1.11 billion (or $0.52 per share) were up 15% from $968 million (or $0.43 per share) at the same point last year.

• Operating ratio increased 310 bps to 59.5%, “including the effect of the tentative union agreements,” CSX said.

• Diluted EPS of $0.52 increased 21% from $0.43 in third-quarter 2021.

2022 Outlook

Looking ahead, CSX reported that it is “still targeting full-year double digit revenue and operating income growth, excluding impacts from the Virginia real estate transaction.” Additionally, it will “continue to increase transportation headcount to restore service,” and is “focused on building a ONE CSX unified company culture to improve relationships with our customers, employees, and all CSX stakeholders.”

“CSX has great potential for profitable growth over the long-term, and my key objective is to help ensure that we realize this opportunity while building a robust organization that will help drive additional value for our customers, our employees and our shareholders,” Hinrichs said.

The Cowen Insight: ‘Sending Foote Off on the Right Note’

“CSX came in above expectations in the third quarter as cost challenges were less apparent (while still hitting margins) compared to Union Pacific (UNP), which brought the group down on Thursday [Oct. 20],” reported Cowen and Company Managing Director and Railway Age Wall Street Contributing Editor Jason Seidl. “Rail service improved sequentially in the third quarter and quarter-to-date as staffing employees appears to be less of a concern vs. the first half of 2022; volumes should be unlocked and tested as service continues to improve. We move our PT to $32 and maintain a Market Perform.”

Key Cowen Takeaways:

• “Third-quarter adjusted EPS of $0.52 came in above our estimate of $0.50 as well as consensus of $0.49. Top-line growth beat our forecast at 18.3% y/y driven by continued yield improvements. Third-quarter adjusted operating ratio (OR) of 59.5% is approximately 130 bps worse than expected and a deterioration from last year’s figure due to labor costs ballooning and an ongoing cost impact from Quality Carriers.

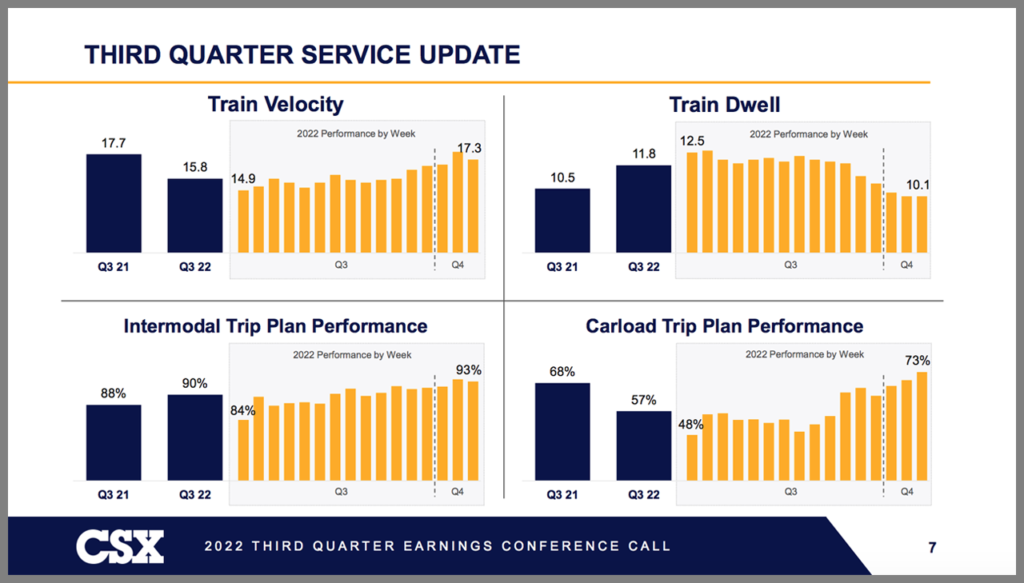

• “Volume growth at 1.5% year-over-year (y/y) remained subdued in the third quarter even as service metrics improved sequentially (though worse on a y/y basis), causing CSX to leave demand on the table. Part of the deterioration is likely due to the short work stoppage that took place in anticipation of a strike in September. It appears that fluidity began showing material improvements toward the beginning of the fourth quarter, though it is unlikely to immediately reflect in volume growth. While coal volumes came under pressure in the third quarter due to mining outages, demand remains robust due to geopolitical factors and is expected to rebound in the fourth quarter. As in the second quarter, autos continue to be a pocket of strength as supply bottlenecks and pent-up demand propel carloads growing 13% y/y; we expect this to continue into the fourth quarter.

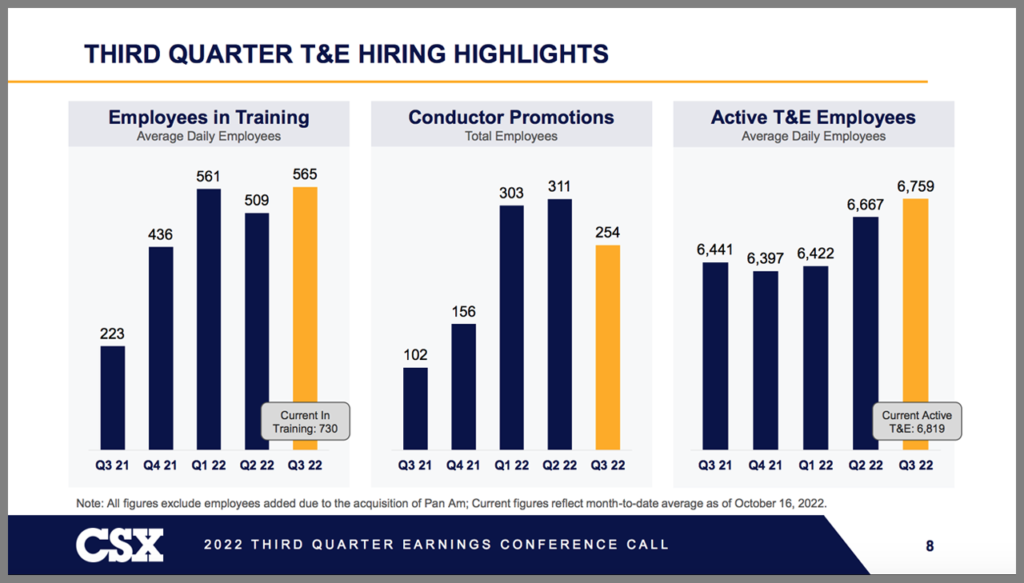

• “Following UNP’s release that broke out labor accruals in the quarter, U.S. rail group sold off on Thursday (among other network issues). CSX stated that labor less the accruals in the quarter should offer a steady run going forward. The hiring pipeline remains robust, and it appears that hiring is starting to sound like less of a concern, in our view. While CSX and the rest of the Class I’s have emphasized hiring, we believe that if the volumes do not come back as rail service continues to improve, the rails may quickly change their tone on and slow the hiring binge, as they have done in the past. This wouldn’t necessarily have to be done by laying off employees, but by slowing the pace of new hires below the attrition rate of approximately 8%-10%.

• “Third-quarter pricing held strong across the board. Intermodal yields continue to be supported by high fuel surcharges though some distress is apparent on the domestic side. Management expressed optimism on pricing power into 2023 despite competition from declining truck spot rates (we note that contract TL rates have not nearly come under the same pressure as spot rates). We remain cautious on whether 2023 pricing power will exceed cost growth due to the reset on the wage base and inflation; management expects ‘sustained inflationary pressure’ in 2023. We model a slight OR deterioration for the year since we anticipate that CSX will be able to take some costs out of the system as network fluidity improves.”